You’re Playing Checkers. Private Equity Is Playing Chess. Here’s What’s Actually Happening.

By Lee Robinson

I was sitting in a room with Pete Moore a few weeks ago. Pete teaches at Harvard on mergers and acquisitions. He’s done dozens of deals in the fitness space. And he was walking a group of gym owners through how private equity actually works.

He put it simply: you’re a gym owner thinking about mortgaging your house to open a second location. Meanwhile, there’s a private equity group that has money from the teachers’ union and Columbia University’s endowment, and they go to the bank and get $16 million without mortgaging anything. They write it into the loan. They show a 27% return multiple and flip it for six times.

And here’s the part that really got the room: who do you think that bank is also working with in real estate? Another PE firm. The capital markets are interconnected. They’re already playing chess while most operators are still playing checkers — especially when it comes to financial reporting, gym revenue optimization, and enterprise-grade club management systems.

📝 Check Out: Year in Review Wellness Watch Report to learn more about what’s impacting the fitness industry.

The Numbers Are Real

In the last 18 months, private equity has deployed more capital into fitness than in the previous five years combined. TSG Consumer Partners acquired EoS Fitness for approximately $1 billion. Leonard Green & Partners bought Crunch for approximately $1.5 billion. L Catterton — backed by LVMH — paid $600 to $700 million for 130 Solidcore studios. Roark Capital merged Orangetheory and Anytime Fitness into Purpose Brands, a $3.7 billion revenue platform with 7,000 locations across 50 countries.

But it doesn’t stop at the big brands. Sixth Street invested $350 million into a single Crunch franchisee. PureGym, backed by KKR, scooped Blink Fitness out of bankruptcy for $121 million. CapitalSpring took a controlling stake in a Michigan-based Crunch franchisee operating 36 units. And EoS — five months after TSG bought them — turned around and acquired 23 Gold’s Gym locations in Southern California from a family that had operated them for 37 years.

Read that again. A family ran 23 gyms for 37 years. Built a great business. And PE-backed EoS acquired them all in a single transaction. That’s not hostile. That’s the math changing. And the math is driven by data analytics, scalable gym management software, and institutional-grade financial infrastructure.

Watch our latest webinar on what’s driving the fitness industry in 2026

The K Inside Fitness

I keep coming back to the K-shaped economy framework because it’s not just about consumers. It’s about who operates and who owns the gyms those consumers walk into.

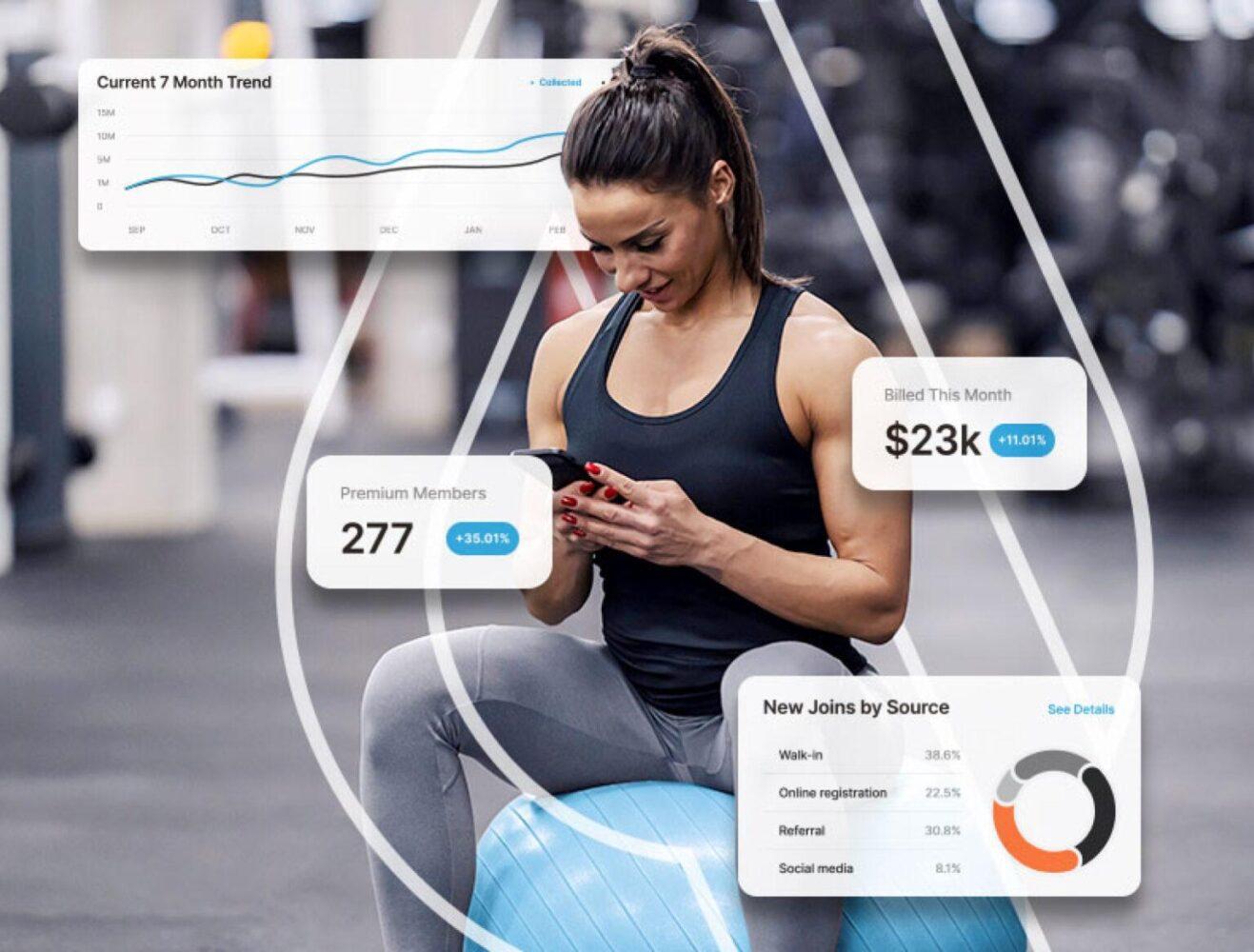

PE firms sit in the top 20% of this K. They have $14 to $70 billion in assets under management. They have operational playbooks from hundreds of portfolio companies. They have data analytics infrastructure, pricing optimization algorithms, and institutional-grade financial reporting. When they look at your gym, they don’t see your community, your members, or the culture you’ve built. They see a cash flow. And they see a cash flow that’s being undermanaged — often because the operator lacks integrated gym billing software, automated payment processing, and real-time performance dashboards.

Most operators sit in the bottom 80%. Not because they’re bad operators. But because they don’t have access to the tools PE firms deploy on day one of every acquisition. They’re managing P&L on spreadsheets. Pricing by gut. Billing monthly and collecting 88% on first attempt. No cohort-level retention data. No segmented lifetime value analysis. No unit-level EBITDA isolation – the kind of insights modern club management systems and gym membership management platforms can deliver.

📝 Check Out: Learn how a Collections ROI Calculator Can Boost Your Revenue

What PE Does in 90 Days

When private equity acquires a gym operator, the first 90 days look the same every time. And every improvement they make is value the previous operator left on the table.

First, billing. They implement intelligent billing systems, powered by integrated gym payment processing and automated recurring billing software, that take collection rates from 88% to 96% or higher. They detect which payment methods are high-risk and configure rules that require backup methods. They use data to predict when members are most likely to have funds available. They time retries accordingly. One operator I’m aware of saw a 7.1 percentage point lift in collection rate just from revenue cycle management — before any AI-driven optimization was even turned on.

Second, labor. They deploy mobile-first operations that let members join, pay past-due balances, book classes, and check in through their phone. That eliminates 2 to 3 front desk FTEs per location at a time when wages have climbed 30% in three years.

Third, pricing. They run price elasticity analysis by cohort and tenure. They raise rates on members who will absorb it and protect at-risk segments. Revenue per member goes up 10 to 15% with negligible churn, especially when supported by data-driven gym management software and advanced reporting tools.

Fourth, reporting. They build the financial package that investment committees require: same-store revenue trendlines, cohort-level retention, revenue per member trajectories, unit-level EBITDA isolation.

Every one of those improvements could have been done by the operator before PE showed up. And every one represents a discount PE baked into the acquisition price.

📝 Check Out: Data-Driven Success: How Analytics Are Reshaping the Future of Fitness in 2025

The Window

Pete Moore talks about a 30-month M&A window that opened in fitness. By his estimate, we’ve got about 12 months left before PE shifts from “buy mode” to “optimize and exit.” That doesn’t mean the opportunity disappears. It means the terms change.

The operators who position now — who build PE-grade financial infrastructure, who can articulate their unit-level EBITDA, who can show a trailing 24-month same-store revenue trendline — will choose their partners and negotiate from strength.

The operators who wait will take what they can get. And some won’t get anything at all.

Which arm of the K are you on?

Next: How the smartest operators are driving up their EBITDA right now — without opening a single new location.

Read the first post in this series here.

Ready to transform your member acquisition strategy? ABC Ignite is the growth-driven gym management platform that streamlines your sales, automates member engagement, and provides the insights you need to optimize every strategy in your toolkit. Get a demo today.